Circle of Life for a Software Bootstrapper

Qualtrics Lands Another PE Investor

The early frontrunner for Deal of the Week is a $12b PE take-private of the publicly traded SaaS company Qualtrics:

The offer values Qualtrics ($XM) at 6.5x their projected 2023 revenue. As GGV’s Jeff Richards points out, this is a good test of where the market perceives fair valuations for public SaaS companies. While the offer is only a 6% premium to the previous day’s closing share price, it represents a healthy 70% increase from where the stock traded in early Jan.

Qualtrics ARR passed $1.5b late in Q4. At that scale, the sweet operating leverage of software should be kicking in. Qualtrics should be minting money, right? Not exactly. In their Q4 earnings release, they said their “non-GAAP operating margin was 6.1%.”

Such a low margin in a scaled software company is catnip to PE firms. They see a bloated business with room for deep cuts to significantly boost margins with minimal impact on growth.

The funny thing about Qualtrics is that, once upon a time, it was a remarkably efficient bootstrapped business. Founded in 2002, they raised a “Series A” from Accel in 2012 - I used quotations because unlike a typical Series A that funds an unprofitable business, Qualtrics was a high-growth, cash gusher.

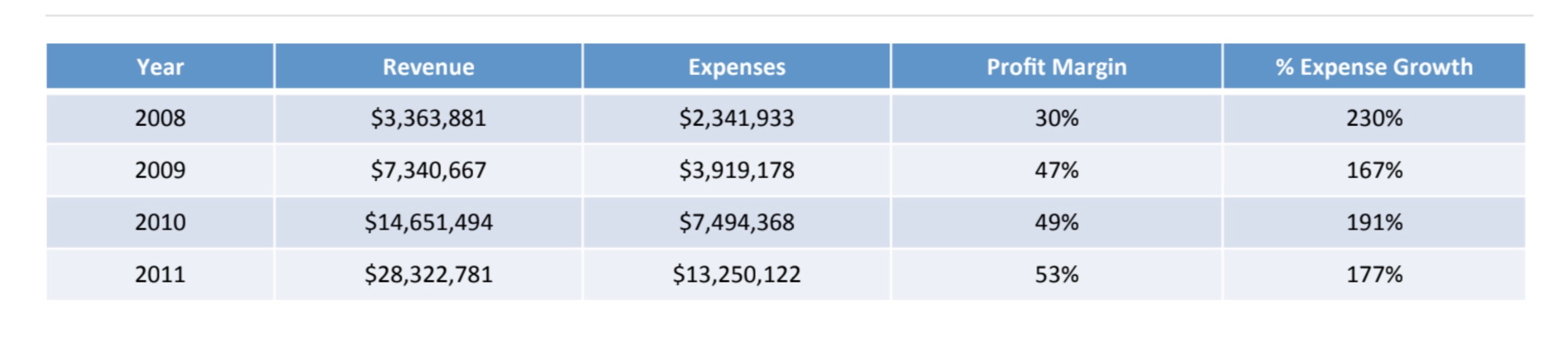

Here are Qualtrics’ financials for 2008-2011:

In 2011, they grew nearly 100% and had a 53% profit margin! That’s a 150 on the Rule of 40.1

What happened?

In 2018, SAP bought Qualtrics for $8b. Accel’s investment was a home run. The founders were thrilled with the outcome. A few years later, SAP spun the company out, so it could run independently as a public company (with SAP maintaining a large stake).

But what happened to those amazing profit margins from 2011?

I don’t know, exactly. But I have a few thoughts:

Transition to SaaS: Qualtrics started out as on-prem, not SaaS. On-prem can actually scale scale more efficiently than SaaS as customer payments are relatively front-loaded. Moving to a SaaS model can take down margins.

Growth over profit: I suspect that after their VC investment, Qualtrics met IPO bankers who told them that the stock market would value growth more than profit. They were right.

Culture change: as bootstrappers, the Qualtrics founders instilled extreme frugality into the company’s culture. That culture undoubtedly changed as the company grew.

This is the Circle of Life for a software bootstrapper. Scale profitably to attract an investor who encourages growth over profit. That mindset is rewarded with a big exit. Later, after the founding culture has gone extinct, a new investor comes along who sees value in cutting costs and restoring the early culture of frugality.

I expect the new PE investors will be successful. The Circle will continue.

These numbers came from the pitch book they put together for a process that led to Accel’s investment.